A loan, originated at the borrower’s doorstep.

A field-ops mobile app for InPrime’s sales and credit teams. Aadhar verification, bank statement analysis, credit bureau check, e-Nach mandate, and disbursement, all stitched into one guided onboarding flow that runs on a phone in tier-2 India.

- Client

- InPrime Finserv

- Industry

- Tech-enabled NBFC

- Engagement

- Custom platform

- Stack

- Flutter · React · Node.js · MySQL

- Status

- Live in production

Lending happens in the field. The software has to follow.

InPrime Finserv is a Bengaluru-based tech-enabled NBFC serving what it calls Informal Prime Households: micro and nano entrepreneurs, self-employed professionals, small retailers, and people in farming and allied sectors. Aspirational borrowers, mostly in tier-2 and smaller markets, who sit outside the credit envelope that traditional lenders comfortably underwrite.

Their growth depends on a sales force that meets these borrowers where they live or run their business and walks them through the entire loan application on the spot. Manual paperwork, branch visits, photocopied documents are not viable at this scale.

The brief was to build the front-of-sales layer of their loan origination system from scratch. A Flutter mobile app for sales and credit teams in the field, a React admin for head office, and a Node.js backend integrating everything an Indian NBFC needs: Aadhar verification, account aggregator, credit bureaus, bank verification, e-mandate, e-sign.

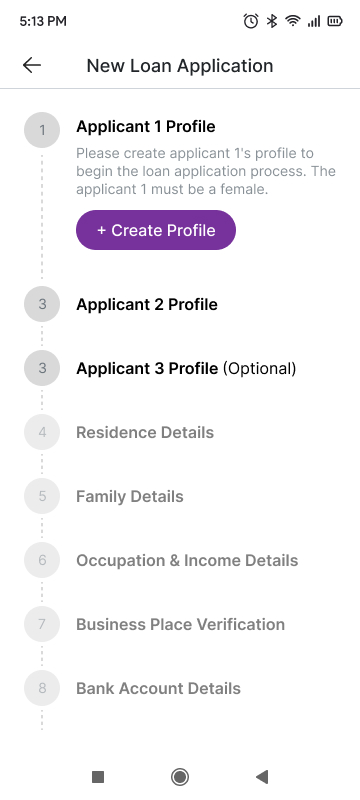

Eight stages. One linear path on the phone.

The full loan origination flow is sequenced as a single guided stepper in the mobile app. Applicant 1, Applicant 2, optional Applicant 3. Residence details. Family details. Occupation and income. Business place verification. Bank account details. The rep walks the borrower through each stage in person, ticks it off, moves on.

Each stage runs its own validations, de-duplication checks and third-party API calls in the background. Account aggregator pull, bank statement analysis, Aadhar verification, OCR on uploaded documents. The rep sees a clean form. The borrower sits across the table watching the process move.

Three things that made this non-trivial.

Field-grade reliability on patchy connectivity

Sales reps work in tier-2 cities where mobile data drops mid-form. The app handles connectivity loss gracefully, queues uploads, never loses captured data, and resumes from where the rep left off. A half-completed loan application is a real loan application. We treated it like one.

Ten-plus integrations stitched into one user flow

Aadhar verification, account aggregator pull, credit bureau check for borrower and co-borrower, penny drop bank match, OCR for document validation, e-Nach mandate (online and offline fallback), Form 16 generation, WhatsApp API for consent. Each one is its own contract, its own latency profile, its own failure mode. The user sees one progressing application.

A credit rule engine that runs on incomplete data

Loan eligibility depends on inputs that arrive in stages. The rule engine evaluates progressively, surfaces a sanctioned amount and max EMI as soon as it has enough signal, and lets the rep keep moving without waiting for every bureau call to come back. Borrowers feel a fluid conversation, not a bureaucratic queue.

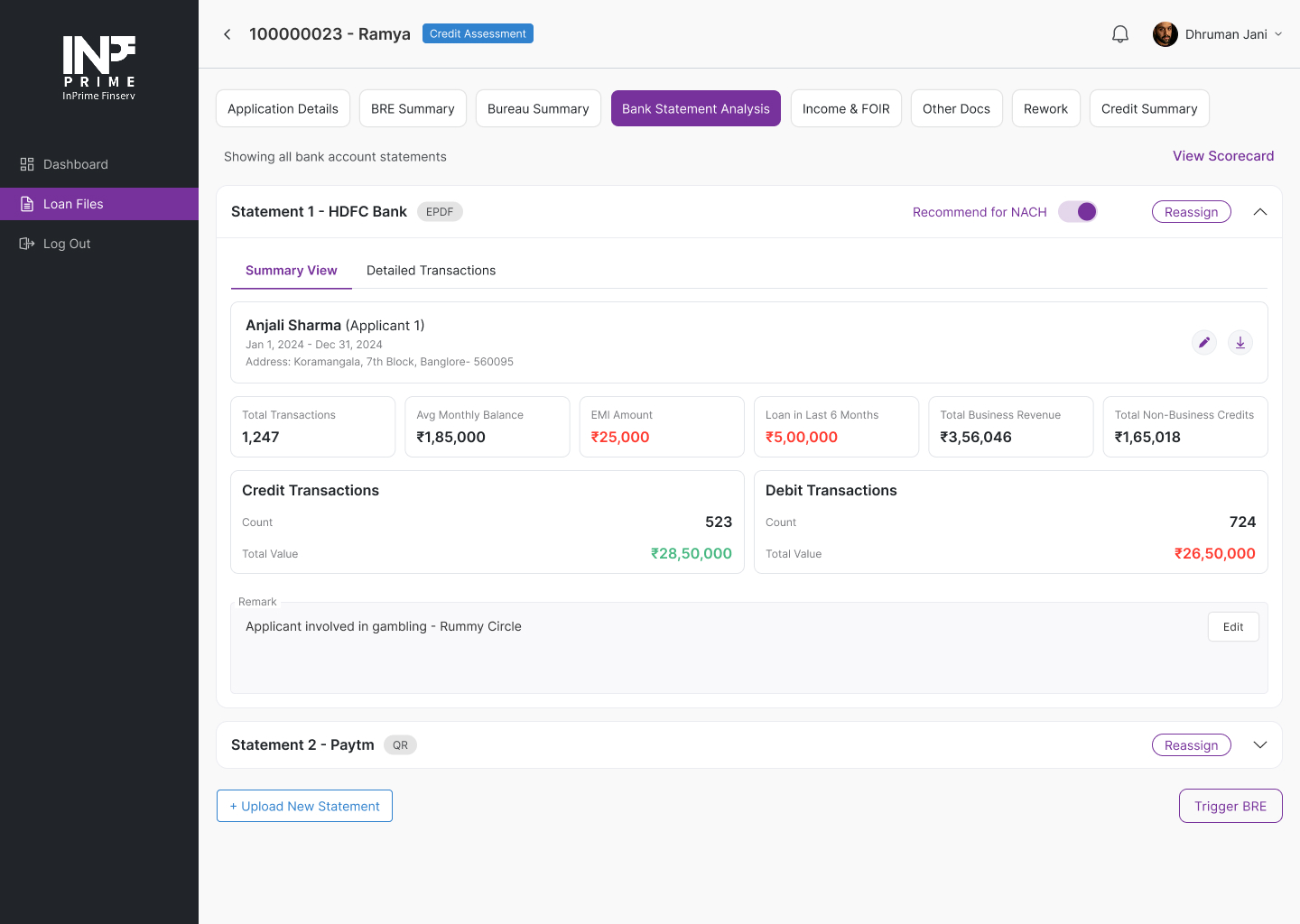

Bank statements, read and reasoned about.

When the borrower’s account aggregator pull comes in, the credit team gets an automated breakdown in the web admin. Total transactions, average monthly balance, EMI amount detected, prior loan exposure across the last 6 months, business revenue versus non-business credits, debits and credits itemised.

Every flag becomes a credit data point. A real applicant’s file once carried the remark “Applicant involved in gambling — Rummy Circle” on it. That kind of signal lives in the statement. The platform surfaces it so the credit team doesn’t have to read every line themselves.

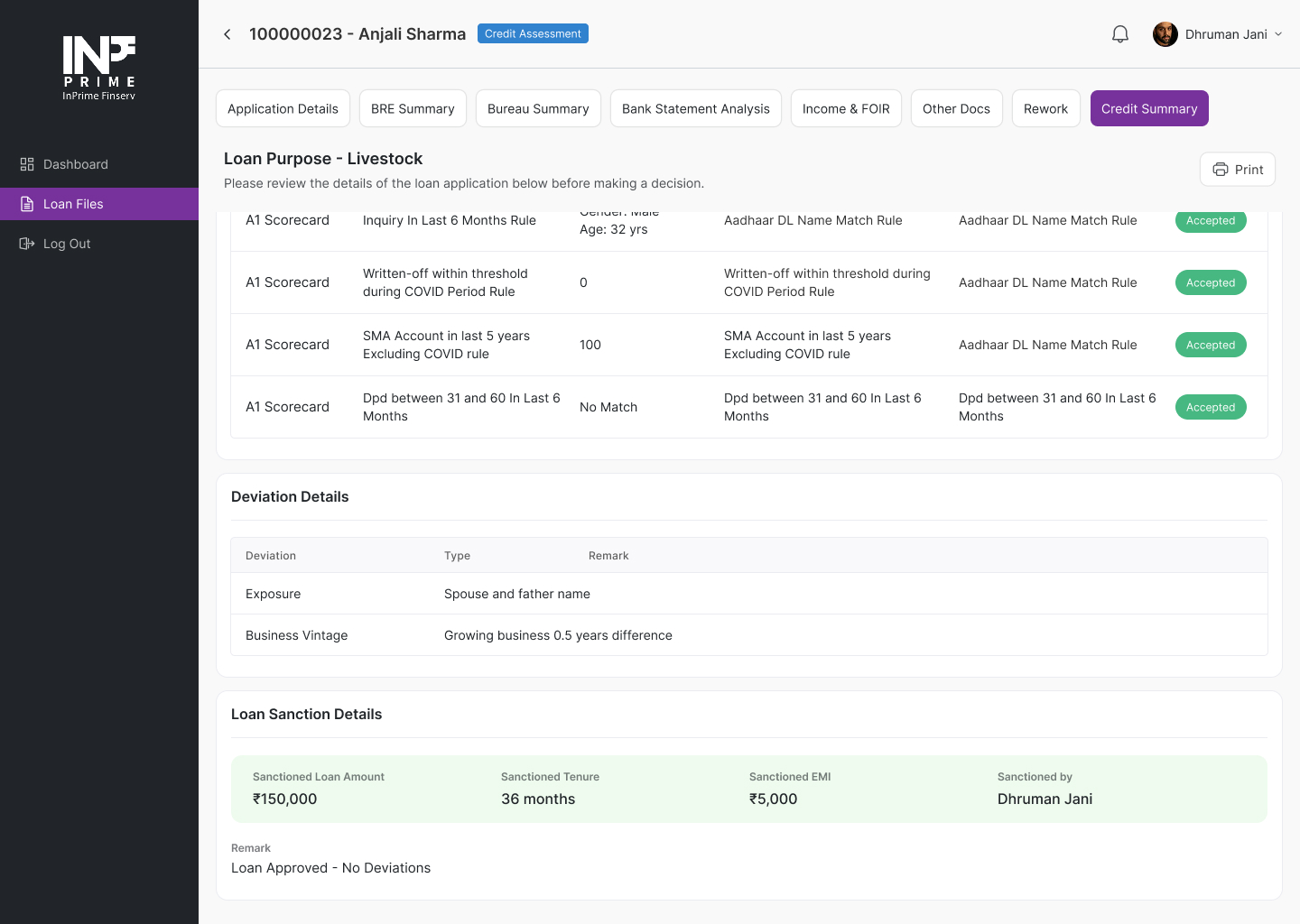

One screen. The whole credit decision.

When all the checks finish, the credit team sees the entire picture in a single page. BRE rule outcomes with accept or reject per rule, deviation details, sanctioned amount, tenure, EMI, and the sanctioning officer’s name. A print button outputs an offer the rep can hand to the borrower then and there.

Decision-to-customer becomes a flow, not a callback. The borrower hears a yes or no on the same visit. Even rejected files come back with reasons the rep can explain on the spot, instead of a generic “we’ll let you know.”

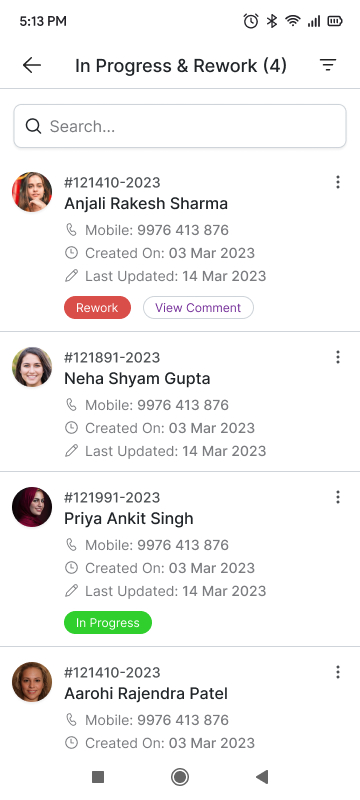

In progress, rework, approved. One queue, on the phone.

Every application has a state. Sales rep working on it. Pending credit team review. Sent for rework with reasons. Approved. Disbursed. The mobile app surfaces the rep’s own queue with a clear status badge per applicant, so they always know which file needs attention before the next field visit.

Behind it, the web admin gives the credit team the same view at portfolio scale, filterable, sortable, with a full audit trail of who touched what when. The same data, two surfaces, no version-of-the-truth arguments at the end of the month.

Six modules. Sales rep to disbursement.

Field sales app

Flutter mobile with login, geolocation tagging, role based access, and the full borrower onboarding sequence as a guided flow.

Identity & KYC

Aadhar verification for borrower and co-borrower, live selfie capture, OCR on uploaded documents, and residence proof module.

Income & banking

Account aggregator pull, automated statement analysis, penny-drop bank verification matched against KYC, Form 16 generation.

Credit decisioning

Bureau check for borrower and co-borrower, progressive credit rule engine, sanctioned amount and max EMI computation, eligibility margin display.

E-mandate & disbursement

Online e-Nach with offline fallback, document e-sign, loan agreement, and live disbursement status updates the rep can show the borrower.

Super-admin web

ReactJS panel with five-KPI dashboard, target segment configuration, role-based authorization for credit teams, and full audit trail.

- Flutter

- React.js

- Node.js

- NestJS

- MySQL

- NGINX

- Account Aggregator

- Credit Bureau APIs

- Aadhar verification

- e-Nach

- e-Sign

- WhatsApp API

- OCR

Live in production.

Used to scale through a Series A1 round.

The platform is live with InPrime’s field sales and credit teams. Sales reps run the full onboarding flow on their phones, head office monitors KPIs from the web admin, and the company keeps adding new loan products and integrations on top of what we built.

In July 2025, InPrime Finserv closed a ₹50 crore Series A1 round led by Pravega Ventures, with participation from Z47, InfoEdge Ventures and Kettleborough VC. The company plans to expand to nearly 50 locations across Karnataka, Uttar Pradesh, Rajasthan and Haryana on top of the platform we built and continue to maintain.

Building a lending platform?

Tell us about it.

Loan origination, KYC stack, account aggregator, bureau integration, e-mandate, field sales app. If your build needs to work in the borrower’s living room on patchy 4G, we have done it before.

Get a free consultation